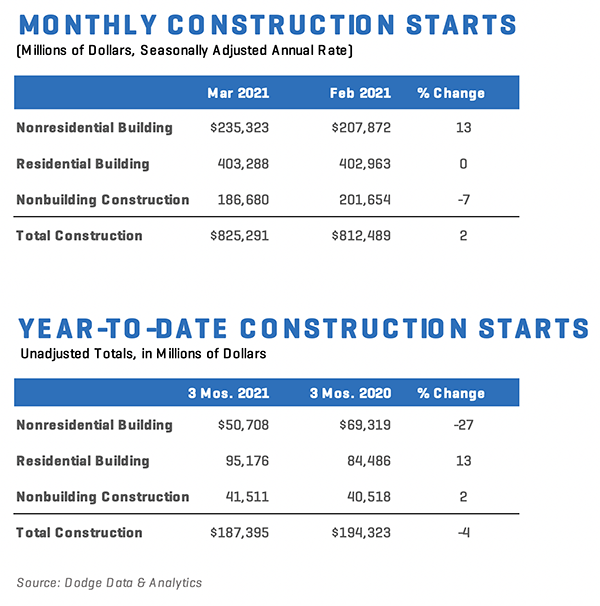

Total construction starts rose 2% in March to a seasonally adjusted annual rate of $825.3 billion, according to Dodge Data & Analytics. A solid gain in nonresidential building starts fueled the March gain, while growth in residential starts was minuscule and nonbuilding starts fell outright. The Dodge Index rose 2% in March, to 175 (2000=100) from February’s 172.

Source: Dodge Data & Analytics

“The March increase in construction starts is certainly welcome news following the past three months of decline,” said Richard Branch, Chief Economist for Dodge Data & Analytics. “Construction will continue to improve as the year moves on. However, just as the pandemic is beginning to loosen its grip on the economy, logistical problems and the rapid escalation in material prices have stepped in as the primary risk to the construction sector. These issues may restrain opportunity in the coming months, causing the sector’s recovery to lag that of the overall economy.”

Below is the full breakdown across nonbuilding, nonresidential, and residential construction:

- Nonbuilding constructionstarts fell 7% in March to a seasonally adjusted annual rate of $186.7 billion, following a sizeable gain in February. Miscellaneous nonbuilding sector (-43%) and environmental public works (-11%) led the decline, whereas the utility gas plant and highway and bridge categories rose 39% and 2% respectively.

For the 12 months ending March 2021, total nonbuilding starts were 10% lower than the 12 months ending March 2020. Highway and bridge starts were 3% higher on a 12-month rolling sum basis, while environmental public works were up 8%. Miscellaneous nonbuilding fell 19% and utility/gas plant starts were down 36% for the 12 months ending March 2021.

The largest nonbuilding projects to break ground in March were the $1.2 billion (1.1 GW) Sanborn Solar Facility in Mojave CA, the $525 million Azure Sky (350 MW) wind farm in Throckmorton TX, and the $425 million Double E Pipeline, a 135-mile pipeline between Eddy County NM and Waha TX.

- Nonresidential building startsrose 13% in March to a seasonally adjusted annual rate of $235.3 billion. Institutional building starts rose 15% during the month fueled by gains in education, recreation, and public buildings. Commercial building starts increased 11% thanks to healthy gains across all commercial sectors. Manufacturing starts, meanwhile, lost 52% in March after strong levels during the previous two months.

For the 12 months ending March 2021, nonresidential building starts dropped 28% compared to the 12 months ending March 2020. Commercial starts declined 30%, institutional starts were down 20%, and manufacturing starts slid 56% in the 12 months ending March 2021.

The largest nonresidential building projects to break ground in March were a $306 million Amazon, Inc. warehouse in Maspeth NY, the $300 million Ball Corp. Aluminum Can factory in Pittson PA, and the $288 million TCCD Northwest Campus Redevelopment in Arlington TX.

- Residential building starts increased by less than one percent in March to a seasonally adjusted annual rate of $403.3 billion. Multifamily starts rose by a brisk 33%, while single family starts slipped 9% lower.

For the 12 months ending March 2021, total residential starts were 6% higher than the 12 months ending March 2020. Single family starts gained 14%, while multifamily starts were down 14% on a 12-month sum basis.

The largest multifamily structures to break ground in March were the $329 million 1629 Market Street mixed-use project in San Francisco CA, the $287 million Schuylkill Yards West Tower in Philadelphia PA, and the $242 million National Urban League mixed-use building in New York NY.

- Regionally, March’s starts rose in the West, South Central, and Northeast regions, but fell in the Midwest and South Atlantic regions.

Related: February sees further decline in national construction starts

{kind=link}