At a seasonally adjusted annual rate of $586.3 billion, new construction starts in July fell 2% from the previous month, according to Dodge Data & Analytics. A steep drop by electric utilities pulled down the nonbuilding construction sector, which in turn contributed to the slight decline for total construction starts.

On the plus side, moderate improvement was reported for nonresidential building, helped by greater activity for its commercial building and manufacturing plant segments, while residential building benefited from a stronger pace by multifamily housing.

During the first seven months of 2016, total construction starts on an unadjusted basis were $372.2 billion, down 11% from the same period a year ago.

- The January-July period of 2015 had featured 13 very large projects valued at $1.0 billion or more, including a $9.0 billion liquefied natural gas export terminal in Texas, an $8.5 billion petrochemical plant in Louisiana, and two massive office towers in New York NY with a combined construction start cost of $3.7 billion.

- In contrast, the January-July period of 2016 included only four projects valued at $1.0 billion or more. Excluding these exceptionally large projects from the comparison leads to a smaller 4% decline for total construction starts year-to-date.

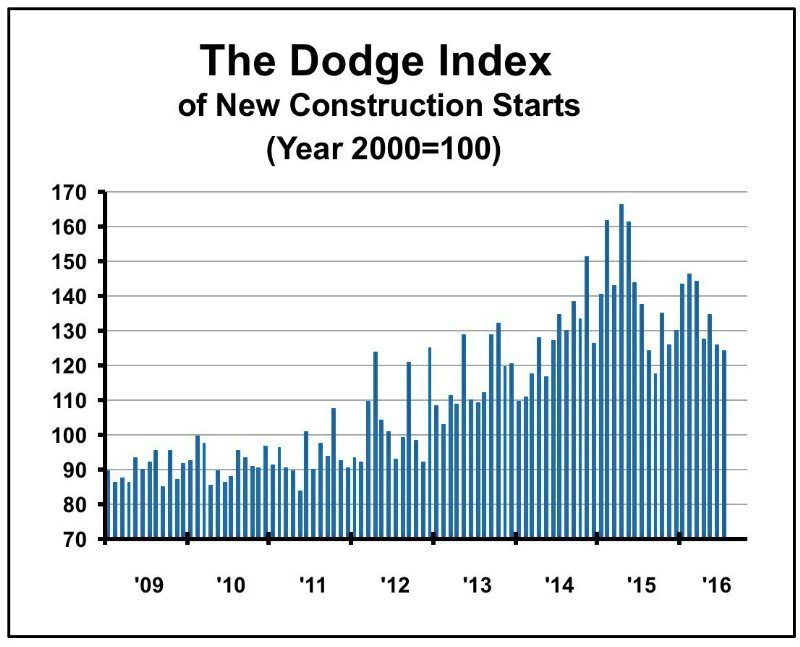

The July data lowered the Dodge Index to 124 (2000=100), down from 126 in June. After the improved pace reported during the first three months of 2016, the construction start statistics showed an up-and-down pattern during the April-June period, and June’s 7% slide has now been followed by the 2% drop in July.

“While the loss of momentum for total construction starts in June and July may raise some concern about the overall health of the construction industry, it’s useful to keep in mind that the recent declines were tied to two segments, public works and electric utilities, that are prone to volatility on a month-to-month basis,” stated Robert A. Murray, chief economist for Dodge Data & Analytics.

“While the loss of momentum for total construction starts in June and July may raise some concern about the overall health of the construction industry, it’s useful to keep in mind that the recent declines were tied to two segments, public works and electric utilities, that are prone to volatility on a month-to-month basis,” stated Robert A. Murray, chief economist for Dodge Data & Analytics.

“June’s retreat for total construction reflected a pullback by public works after a strong performance in May, and July’s retreat for total construction reflected a subdued amount of electric utility starts for that month. At the same time, nonresidential building was able to register moderate growth in June and July, while residential building can be viewed as essentially stable when taking the average of June and July.”

Murray continued, “The year-to-date comparisons so far in 2016 have been skewed by the number of exceptionally large projects that reached the construction start stage during the first half of 2015. There were fewer such projects during the second half of 2015, which should help the year-to-date comparisons as 2016 proceeds. It’s true that the July statistics showed only slight improvement with the year-to-date comparisons, but that improvement should become greater with the August and September construction start reports. This is due to the fact that last year August and September witnessed a broader slowdown for construction starts, as investment grew more cautious given concerns about the global economy and the continued drop in energy prices. This year the uncertainty related to energy prices has diminished, with the price of oil hovering in the range of $40 to $50 per barrel. Admittedly though, this year has a new element of uncertainty with regard to the upcoming November elections, which conceivably could dampen some investment in the very near term.”

July 2016 construction starts

Source: Dodge Data & Analytics

Nonbuilding construction

Nonbuilding construction in July plunged 17% to $121.7 billion (annual rate).

The electric utility and gas plant category fell 56% in July, while public works as a group was unchanged from the previous month. July’s steep drop for electric utilities and gas plants reflected the comparison to June’s elevated amount, which included three huge natural gas-fired power plants located in Tennessee ($975 million), New York ($900 million), and New Jersey ($600 million).

In contrast, the power plant projects that were entered as July starts were generally smaller in scale than what was reported in June, as July’s largest power plant projects were a $385 million solar power facility in California and three wind farms located in California ($300 million), North Dakota ($250 million), and Minnesota ($135 million). The public works group in July showed a mixed performance by category.

On the plus side, sewer construction jumped 86%, supported by the start of the $415 million EchoWater biological nutrient removal project in California. Water supply construction advanced 48%, lifted by the start of four water main projects totaling $376 million in Chicago IL.

On the negative side, decreased activity was reported in July for highways and bridges, down 8%; river/harbor development, down 8%; and miscellaneous public works (site work, rail projects, pipelines, etc.), down 29%.

Nonresidential building

Nonresidential building, at $187.9 billion (annual rate), grew 4% in July following its 7% gain in June. The commercial building group advanced 3%, with much of the lift coming from a 20% jump for office construction. Large office building projects that reached groundbreaking in July were the following – a $400 million data center in Grand Rapids MI, a $133 million office building in Dallas TX, and the $100 million Comcast office building at Sun Trust Park in Atlanta GA.

During the first seven months of 2016, the top five metropolitan areas ranked by the dollar amount of office construction starts were – New York NY, Washington DC, Dallas-Ft. Worth TX, Atlanta GA, and San Francisco CA. Store construction in July improved 3%, helped by the start of the $50 million Simon Premium Outlet Mall in Norfolk VA. New warehouse starts in July slipped 6% and a 14% drop was reported for hotels, although July did include the start of the $100 million Maryland Live Casino Hotel in Hanover MD and the $100 million renovation of the Phoenician Resort in Scottsdale AZ.

During the first seven months of 2016, the top five metropolitan areas ranked by the dollar amount of office construction starts were – New York NY, Washington DC, Dallas-Ft. Worth TX, Atlanta GA, and San Francisco CA. Store construction in July improved 3%, helped by the start of the $50 million Simon Premium Outlet Mall in Norfolk VA. New warehouse starts in July slipped 6% and a 14% drop was reported for hotels, although July did include the start of the $100 million Maryland Live Casino Hotel in Hanover MD and the $100 million renovation of the Phoenician Resort in Scottsdale AZ.

The manufacturing building category increased 89% in July after a weak June, lifted by the start of a $350 million pharmaceutical research facility in East Windsor NJ and a $154 million plant for an automotive systems supplier in Cottondale AL.

Institutional activity

The institutional side of the nonresidential building market eased back 1% in July. Reduced activity was reported for educational facilities, down 5%, although July did include the start of a $150 million computer science building at the University of Maryland in College Park MD, a $130 million high school in Pinole CA, and a $129 million high school in Secaucus NJ.

Healthcare facilities also showed reduced activity in July, slipping 4%, despite the start of a $250 million critical care facility in Tallahassee FL and the $239 million Bayhealth medical campus in Milford DE.

The smaller institutional categories witnessed gains in July, with public buildings up 5%, churches up 8%, amusement and recreational facilities up 11%, and transportation terminals up 11%. The transportation terminal category was boosted by the $295 million Terminal 1 Concourse A and connector bridge addition at Ft. Lauderdale-Hollywood International Airport in Ft. Lauderdale FL.

Residential building

Residential building in July increased 3% to $276.7 billion (annual rate), rebounding after the 3% decline reported in June. Multifamily housing provided the upward push, rising 9%. July included eight multifamily projects valued at $100 million or more, led by the $485 million Brickell Flatiron high-rise in Miami FL, a $275 million apartment high-rise in Chicago IL, and a $250 million luxury condominium high-rise in New York NY.

During the first seven months of 2016, the top five metropolitan areas ranked by the dollar amount of new multifamily starts were – New York NY, Miami FL, Chicago IL, Los Angeles CA, and Boston MA. The New York NY share of the national dollar amount of multifamily starts was 22% so far in 2016, down slightly from the 26% share for the full year 2015.

During the first seven months of 2016, the top five metropolitan areas ranked by the dollar amount of new multifamily starts were – New York NY, Miami FL, Chicago IL, Los Angeles CA, and Boston MA. The New York NY share of the national dollar amount of multifamily starts was 22% so far in 2016, down slightly from the 26% share for the full year 2015.

Single family housing in July increased 1%, basically extending the plateau present during the first half of 2016. The regional pattern for single family housing in July showed increases in three regions – the Northeast, up 8%; the West, up 6%; and the South Atlantic, up 2%; while declines were reported in the Midwest, down 2%; and the South Central, down 5%.

The 11% decline for total construction starts on an unadjusted basis during the January-July period of 2016 was due to diminished activity for both nonbuilding construction and nonresidential building from their heightened levels of a year ago. Nonbuilding construction dropped 21% year-to-date, with public works down 14% and electric utilities/gas plants down 33%. Nonresidential building dropped 18% year-to-date, with commercial building down 7%, institutional building down 12%, and manufacturing building down 66%.

Residential building was the one major sector to show a year-to-date increase, rising 2% with single family housing up 7% while multifamily housing retreated 9%. By geography, total construction starts during the first seven months of 2016 revealed this pattern relative to a year ago – the South Central, down 31%; the Northeast, down 16%; the West, down 2%; the South Atlantic, down 1%; and the Midwest, up 3%.

| July 2016 Construction Starts | ||||||||||||||||

| Monthly Summary of Construction Starts | ||||||||||||||||

| Prepared by Dodge Data & Analytics | ||||||||||||||||

| Monthly Construction Starts | ||||||||||||||||

| Seasonally Adjusted Annual Rates, in Millions of Dollars | ||||||||||||||||

| July 2016 | June 2016 | % Change | ||||||||||||||

| Nonresidential Building | $187,883 | $180,954 | +4 | |||||||||||||

| Residential Building | 276,732 | 268,168 | +3 | |||||||||||||

| Nonbuilding Construction | 121,689 | 146,490 | -17 | |||||||||||||

| Total Construction | $586,304 | $595,612 | -2 | |||||||||||||

| The Dodge Index | ||||||||||||||||

| Year 2000=100, Seasonally Adjusted | ||||||||||||||||

| July 2016 ….…..124 | ||||||||||||||||

| June 2016………126 | ||||||||||||||||

| Year-to-Date Construction Starts | ||||||||||||||||

| Unadjusted Totals, in Millions of Dollars | ||||||||||||||||

| 7 Mos. 2016 | 7 Mos. 2015 | % Change | ||||||||||||||

| Nonresidential Building | $111,800 | $135,864 | -18 | |||||||||||||

| Residential Building | 163,577 | 160,679 | +2 | |||||||||||||

| Nonbuilding Construction | 96,852 | 122,577 | -21 | |||||||||||||

| Total Construction | $372,229 | $419,120 | -11 | |||||||||||||

| Total Construction, excluding projects valued at $1 billion or greater | ||||||||||||||||

| $357,344 | $372,527 | -4 | ||||||||||||||

About Dodge Data & Analytics: Dodge Data & Analytics is a technology-driven construction project data, analytics and insights provider. Dodge provides trusted market intelligence that helps construction professionals grow their business, and is redefining and recreating the business tools and processes on which the industry relies. Dodge is creating an integrated platform that unifies and simplifies the design, bid and build process, bringing data on people, projects and products into a single hub for the entire industry, from building product manufacturers to contractors and specialty trades to architects and engineers. The company’s products include Dodge Global Network, Dodge SpecShare, Dodge BuildShare, Dodge MarketShare, and the ConstructionPoints and Sweets family of products. To learn more, visit www.construction.com.

SOURCE Dodge Data & Analytics

{kind=link}